Tracking loans and mortgages in TallyMint

A loan in TallyMint is an account that knows its own math. You give it the terms once (rate, payment, payment day) and it computes the full amortization schedule from what you owe today to the final payment. When you record a payment, TallyMint splits principal and interest for you, so the loan balance and your spending reports both stay right without a calculator.

Step 1: Create the loan account

Add an account with the Loan type and enter what you currently owe as the opening balance. It shows in the sidebar as a negative balance, because it is money you owe, and it feeds the Net Worth report as a liability.

Step 2: Attach the loan terms

Open the loan account and enter the terms:

- Annual rate %: the loan's interest rate.

- Monthly payment: the regular principal-and-interest payment. For a mortgage, use just the principal and interest portion, not escrow; taxes and insurance are ordinary categorized spending.

- Payment day of month: when the payment is due.

- Interest category: where interest lands in your spending (for example a Mortgage Interest category, handy at tax time).

- Original amount (optional): the amount you first borrowed, for the payoff progress display.

The schedule is computed from the account's current balance forward, so a loan you are five years into is entered in seconds; no need to reconstruct history.

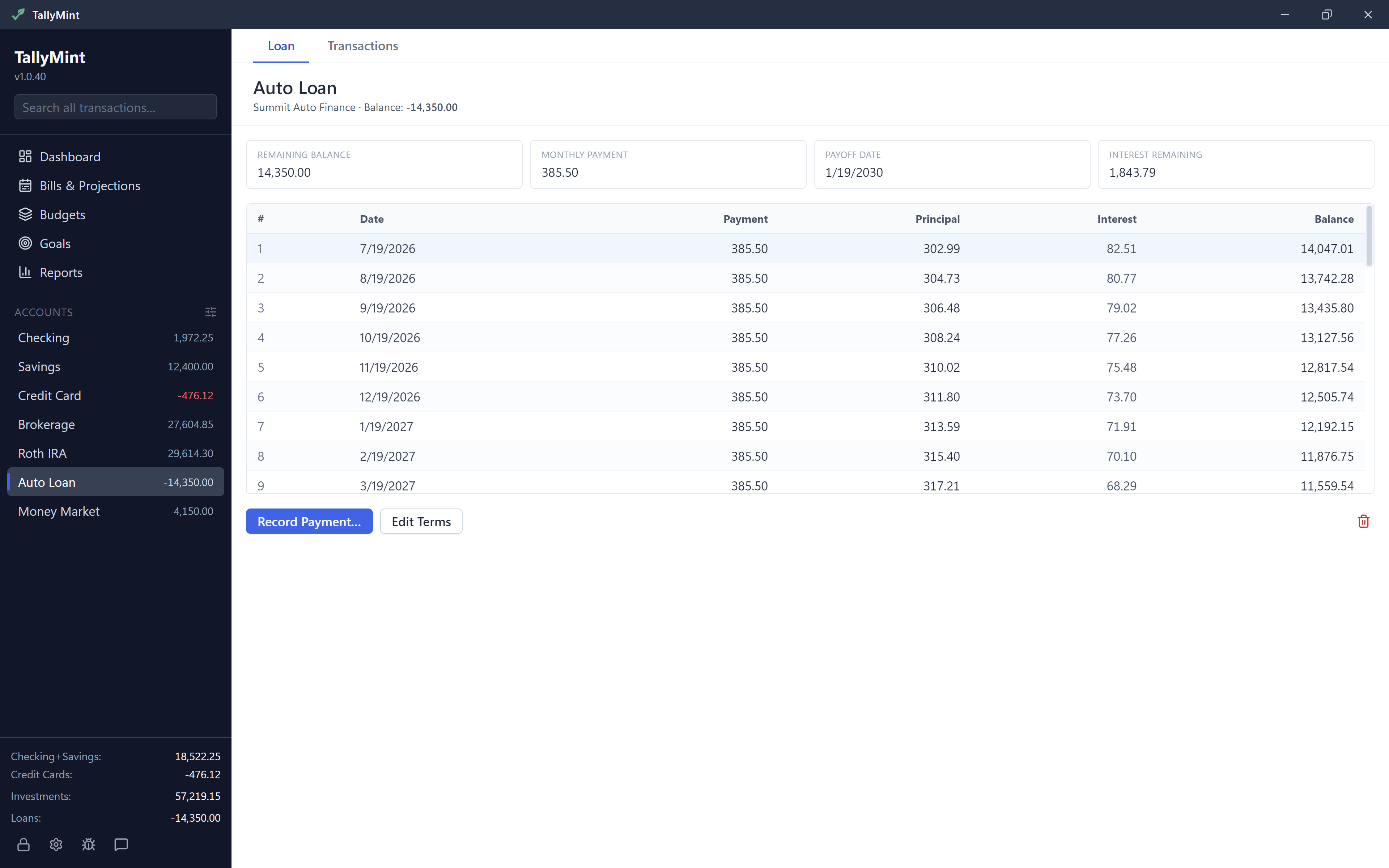

Step 3: Read the schedule

The schedule lists every payment between now and payoff with its principal portion, interest portion, and the balance after. Above it, summary chips show the remaining balance, monthly payment, and total interest remaining. If the payment you entered does not cover the interest, TallyMint says so plainly instead of showing a schedule that never ends.

Step 4: Record payments

When a payment happens, use Record Payment:

- Pick the account the payment comes from (usually checking) and confirm the total and the interest portion; TallyMint pre-fills them from the schedule, and the principal is derived automatically.

- TallyMint then books two things at once: the interest as spending in your interest category, and the principal as a transfer from the funding account to the loan, which reduces what you owe.

That split is the part loan tracking usually gets wrong when done by hand. Booked this way, your checking account drops by the full payment, the loan balance falls by exactly the principal, and only the interest counts as spending in reports and budgets.

Tips

- Add a recurring bill for the payment so it appears in your bills calendar and balance forecast.

- Extra principal payments are just a transfer from checking to the loan; the schedule recomputes from the new balance and shows the payoff coming sooner.

- Mark the interest category tax-relevant in Settings > Categories and mortgage interest shows up in the Tax Report.